Strait of Hormuz Crisis: How the Iran War Is Driving Oil Prices and Global Inflation

Strait of Hormuz Crisis: How the Iran War Is Driving Oil Prices and Global Inflation

Global Markets at a Crossroads: War, Inflation, and Fragmentation? And industries that thrive or barely survive!

Strait of Hormuz Crisis: A Supply Shock, Not a Demand Cycle

The current global market environment is being shaped by a rare convergence of geopolitics, inflation risk, and policy constraint. The ongoing U.S.-Israel war against Iran has triggered a severe disruption in global energy markets through the effective closure of the Strait of Hormuz, a passage responsible for 20% of global oil supply. This is not a typical cyclical downturn, rather, it’s a negative supply shock, meaning:

- Prices rise while growth slows

- Central banks lose flexibility

- Volatility increases across asset classes

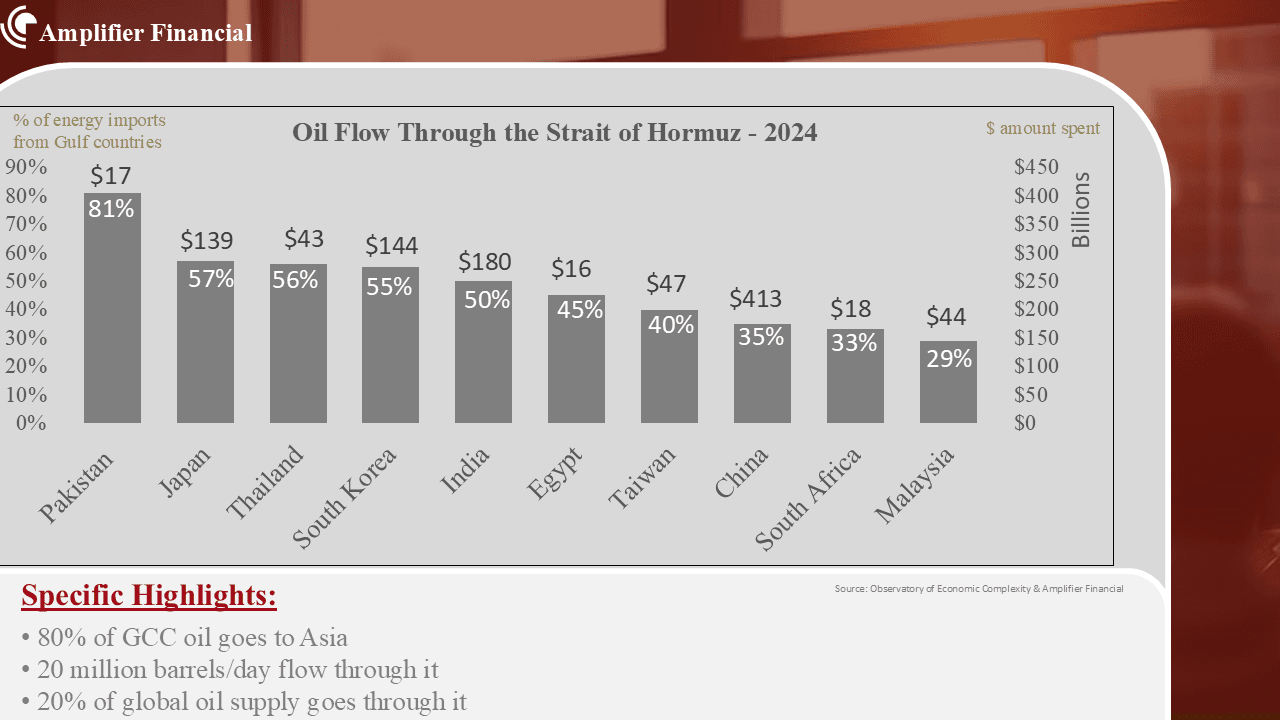

20 million barrels/day flow through the Strait of Hormuz, and roughly 80% of that goes to Asia. As a result, oil prices have surged above $100/barrel and it’s likely to significantly increase if disruptions persist.

Asia serves as the primary conduit through which the shock propagates across the global economy, which amplifies its impact far beyond the region. Therefore, manufacturing costs rise sharply due to increased input prices and energy constraints, which in turn pushes export prices higher across international markets. At the same time, fragile supply chains become even more constrained, with delays, bottlenecks, and reduced efficiency compounding the disruption. Given Asia’s central role in global production and trade, these effects do not remain localized, but instead ripple outward, which affects both developed and emerging economies alike. This is precisely why the shock cannot be viewed as a regional disturbance as it is global in scope and systemic in its consequences, with the potential to reshape trade flows, inflation dynamics, and economic stability worldwide.

Upward Inflationary Pressure

The OECD now expects higher global inflation and weaker growth, and it warns that this may accentuate stagflation. This war is feeding directly into inflation through multiple channels:

- Energy: rising energy prices directly increase the cost of fuel, electricity, and transportation which creates broad-based inflationary pressure across both consumers and businesses.

- Fertilizers: higher fertilizer costs drive up agricultural production expenses, which ultimately translate into elevated food prices globally.

- Petrochemicals: increased petrochemical input costs raise the price of plastics and a wide range of industrial goods, which impacts manufacturing margins and end-product pricing.

- Logistics: disruptions in logistics lead to higher shipping rates and insurance costs, which further amplifies the overall cost of moving goods across global supply chains.

The Fed: Trapped Between Inflation and Growth

A sharp surge in energy markets, where crude oil prices have already risen by more than 40%, has intensified inflationary risks, which makes it difficult for the Fed to pivot toward easing. As a result, interest rates remain elevated in the range of roughly 3.5%-3.75%, with anticipated rate cuts being delayed and markets even beginning to price in the possibility of renewed hikes. The Federal Reserve (Fed) is constrained and can no longer support financial markets. historically, such an environment tends to be bearish for equities (particularly growth stocks).

Trade Fragmentation

Economic nationalism is on the rise due to geopolitical shock, another structural force. Trade barriers introduced and/or expanded under the Trump administration would continue to :

- increase input costs

- reduce global efficiency

- and Accelerate globalization and nearshoring

combined with war-driven supply shocks, this may lead to

- structurally higher inflation

- lower long-term productivity

- and fragmented global supply chains

Industries Likely to perform well vs poorly

| Winners | Losers |

| Energy | Airlines & Travel |

| Defense & Aerospace | Chemicals & Fertilizers |

| Commodities & Materials | Autos & Industrials |

| Shipping | Consumer Discretionary |

| Renewables & Energy Transition | Semiconductors (Short-Term) |